11 Questions About Jewelry Insurance

Visit our insurance partner, Jewelers Mutual, and Get a Quote today!

We tend to insure the most expensive things we own, such as our cars or our homes, but what about our jewelry?

Jewelry insurance is an unknown concept to many people, even though an engagement ring is among one of the most expensive things you will buy or own in your lifetime. An engagement ring or wedding ring is also highly susceptible to damage or loss, as it is worn daily, increasing the risk of something happening to it.

Even if you don’t wear your jewelry out, it isn’t exactly safe at home. In fact, it is one of the most commonly stolen items out of homes. So what can you do to protect your investment? Read on to find answers to some of the most common questions about jewelry insurance.

1. Do I really need jewelry insurance? Is jewelry insurance worth it?

If you have a valuable or sentimental piece of jewelry, like an engagement ring, wedding ring, or anniversary ring, it is worth looking into jewelry insurance. It’s easy for jewelry to go missing – we often take off our rings to wash our hands, put on lotion, or go swimming. Some people end up wearing their engagement rings as little as possible out of fear of something happening to it. This shouldn’t be the case – jewelry is meant to be worn and enjoyed, especially a beautiful ring that your partner bought for you.

Even though every Ritani engagement ring automatically comes with a Ritani Lifetime Care Package, you should still consider insurance. The Ritani Lifetime Care Package includes a warranty for your ring, but this only includes repairs. It does not cover loss or theft. Luckily, getting jewelry insurance and filing a claim is usually very easy online.

2. What exactly does jewelry insurance cover?

Insurance companies will give you different options to insure your jewelry. A good insurance plan will cover the full value of your jewelry in the event of damage, theft, accidental loss, and mysterious disappearance. A jewelry insurance policy that promises to cover the full cost of your jewelry will almost always include sales taxes as a part of your coverage.

Insurance terms can get a little confusing, so let’s dissect them.

Mysterious Disappearance

“Mysterious disappearance” is when your jewelry goes missing, but you are unsure if it was stolen or misplaced. Petty theft can go unnoticed for months.

Let’s say you own a vintage diamond necklace that you only wear for special occasions. You store it in your jewelry box and don’t wear it for another few months. Eventually, you’re invited to a party and you decide to wear your vintage diamond necklace. Soon you realize – my necklace disappeared! It’s nowhere to be found in your home. In the few months that you didn’t wear the necklace, it could have been stolen and you just never noticed. This is a case of mysterious disappearance.

Accidental Loss

You may be wondering what the difference is between accidental loss and mysterious loss. It sounds pretty similar, right? Accidental loss is when you’ve lost your jewelry by mistake, or it has become irreplaceable in an accident. Let’s say you have a beautiful pearl necklace. You put it on, drive to work, and you get in a car accident. The airbag deploys, your necklace breaks, and pearls are everywhere. You later find out there is no way to repair the necklace. This situation is considered accidental loss because the necklace is damaged beyond repair. Luckily, if you have jewelry insurance (and hopefully car insurance, too), your insurance will cover the losses.

Coverage Area

It’s also important to make sure your coverage is worldwide, so if you travel outside of the country and lose your jewelry, it can still be replaced. It’s easy to misplace things when you’re traveling, and tourists can easily become victims of theft because they don’t know the area well.

3. How much does jewelry insurance cost?

Like car insurance, your rate will vary on usage (how often you wear it), where you live, and your insurance plan’s deductible. Typical rates for insuring jewelry usually come in around 1-2% of the jewelry’s value. For example, if you bought a ring for $6,000, it may only be $60 a year to insure - that's only $5 a month!

4. Does my homeowner’s insurance or renter's insurance cover my jewelry?

This is without a doubt the most common misconception about insuring jewelry. While many homeowner’s insurance policies do deal somewhat with jewelry, it is considered a “non-essential” household item. Non-essential household items tend to get the short end of the stick when it comes to homeowner’s insurance.

It typically covers up to $1,000-$2,000 – so if your $6,000 ring gets stolen, they won’t reimburse you for its full value. (I know, it sucks.) Additionally, they usually don’t cover jewelry that is simply lost. This is typically the same with renter's insurance - renter's insurance won't cover the full value of your jewelry.

If your jewelry is stolen outside of the home, like in a hotel room, your homeowner’s insurance won’t cover it. It is important to go through your policy and understand what your homeowner's insurance or renter's insurance actually covers before deciding whether or not you should invest in jewelry insurance.

Say you owned a gorgeous pair of sapphire earrings valued at $3,000, and these earrings were stolen in a burglary. Like it or not, jewelry is one of the most frequently stolen items in America, since it is expensive and easy to carry. Under most standard homeowner’s insurance policies, there is an incredibly low cap for the monetary value of your jewelry. If your homeowner’s insurance allowed you to be reimbursed at all, it would be for a fraction of the earrings’ actual value.

5. Can I buy a blanket policy for my entire collection, or do I have to insure individual items?

In terms of what jewelry to insure, I strongly recommend that customers insure their engagement rings separately. They are high-value pieces that are worn every day, so it is more likely that something will happen to them.

Of course, you can also buy a blanket policy for all of your jewelry. The only requirement is having your pieces appraised so the jewelry insurance company knows the replacement value of your collection.

6. How often does my jewelry need to be appraised?

Even though a Ritani engagement ring or jewelry piece will come with a free expert appraisal, jewelry should be appraised around every three to five years. It’s important to get your jewelry appraised this often because the jewelry market is always changing. Luckily, jewelry appraisals are typically quite inexpensive!

Prices for certain stones can change from year to year. Inflation changes can also change the value of your jewelry. Getting the correct value of your jewelry is important for proper insurance coverage.

module

7. How should I keep my jewelry safe?

You should consider investing in a safe to store your jewelry in when you’re not wearing it. Doing so can keep the costs of your insurance down. You should take photos of the process and describe where it is in your house so you can show your insurance you are not being careless with your valuables.

The first place a burglar looks is usually the bedroom because it is where most people store their valuables. If you’re very concerned about your jewelry being stolen, you may want to consider a sneakier place to store your safe.

8. Do I have to buy extra traveler’s insurance to cover my jewelry when I’m abroad?

No need, if your plan is comprehensive. Just like extended coverage for your phone, jewelry insurance travels with you even if you are out of the country. A good jewelry insurance plan will make no distinction between losing a diamond earring at work and losing an earring while skiing in the Alps. Always make sure to read your policy before you travel.

9. What is the jewelry insurance claim process like?

Insurance claims for jewelry go through a very similar process to car insurance claims. A policy agent will assign you a claim number and you will be asked to provide any relevant photos, police reports, and documentation about your stolen jewelry.

Two documents that will be essential to filing a jewelry insurance claim are a value appraisal for the stolen piece and, if it is a piece of diamond jewelry, the center diamond’s GIA or AGSL certification report. If you purchased your ring from a reputable jeweler, there’s no need to worry if you lost your appraisal or diamond grading report. You should be able to request another appraisal and the grading laboratories should have no problem sending you a replacement report.

10. What happens if I find the jewelry I filed a claim for?

It happens all the time – you think your jewelry is gone for good, you file an insurance claim, and then a few months later, you find your lost jewelry. If you’ve found the jewelry that you filed a claim for, contact your insurance. In most cases, you will either have to pay the money back to your insurer or return the new piece you bought with the insurance money to your insurance company.

Failing to notify your insurer that you found jewelry you filed a claim for is insurance fraud, which is a criminal offense. It’s not worth spending possible jail time over. Contact your insurance company and be honest about what happened.

11. How do I get the most out of my jewelry insurance?

In order for your jewelry insurance plan to be truly worth its cost, you must reassess it from time to time. My recommendation is this: every year, before you do your taxes, spend some quality time with your jewelry collection. Note any new pieces you acquired throughout the year, and evaluate your pieces that are currently insured.

As the market value for certain jewelry materials fluctuates from year to year, so will the value of your jewelry. You should take special care to double-check that the market values of loose diamonds and gold jewelry have not increased or decreased significantly. You can use this information to adjust your policy accordingly.

How to Insure Jewelry

To insure your jewelry, you will need a detailed appraisal. A diamond grading report is not enough; a report simply describes the quality of the diamond, but not its value.

It’s best if the appraisal is no more than 5 years old since the value of your jewelry can fluctuate. While many jewelry insurance companies do not require the appraisal upfront to get coverage on your jewelry, you will need to present the appraisal if your jewelry is lost, goes missing, or is stolen. The more detailed your appraisal, the better. Your appraisal, which should be printed on the appraiser’s business letterhead, should include:

- Diamond information such as shape, cut, color, clarity, and carat weight

- Information on side stones (if applicable)

- A description of the jewelry

- The type of metal used for the jewelry (for example, 14kt white gold, platinum, etc.)

- The value of the piece

- The appraiser’s contact information

To get an accurate appraisal, make sure to consult a jeweler with training from a reputable agency like the GIA or AGS.

Once you’ve garnered your appraisal, it’s time to find the right insurer.

Getting the Right Insurance

Getting jewelry insurance online is fast and easy. You'll be asked to fill out basic information to receive a quote, like where you live and the value of your jewelry piece. We recommend getting quotes from various companies before settling on one company.

In order to get the best insurance, you’ll want to make sure you fully understand its coverage. Fully understanding what your insurance covers will help you protect your ring better and give you greater peace of mind.

You never know what the future holds, and it’s better to have coverage for whatever life throws at you. As they always say – better safe than sorry.

RELATED: 9 Things You Should Be Doing to Take Care of Your Ring

DISCLAIMER

Jewelers are not licensed agents and do not sell or offer advice about insurance. Insurance coverage is offered by a member insurer of the Jewelers Mutual Group, either Jewelers Mutual Insurance Company, SI (a stock insurer) or JM Specialty Insurance Company. Policyholders of both insurers are members of Jewelers Mutual Holding Company. Any coverage is subject to acceptance by the insurer and to policy terms and conditions.

February 9, 2023

What You Need To Know About Caring For Your Diamond Jewelry

Do you have questions about diamond jewelry maintenance? Here’s a helpful and detailed guide on what you need to know about caring for your diamond jewelry.

Read article

September 14, 2021

How Thick Or Thin Should My Engagement Ring Be?

Dainty engagement rings are trendy, but may not last in the long run. Here's our tips for choosing the right engagement ring band size.

Read article

September 19, 2025

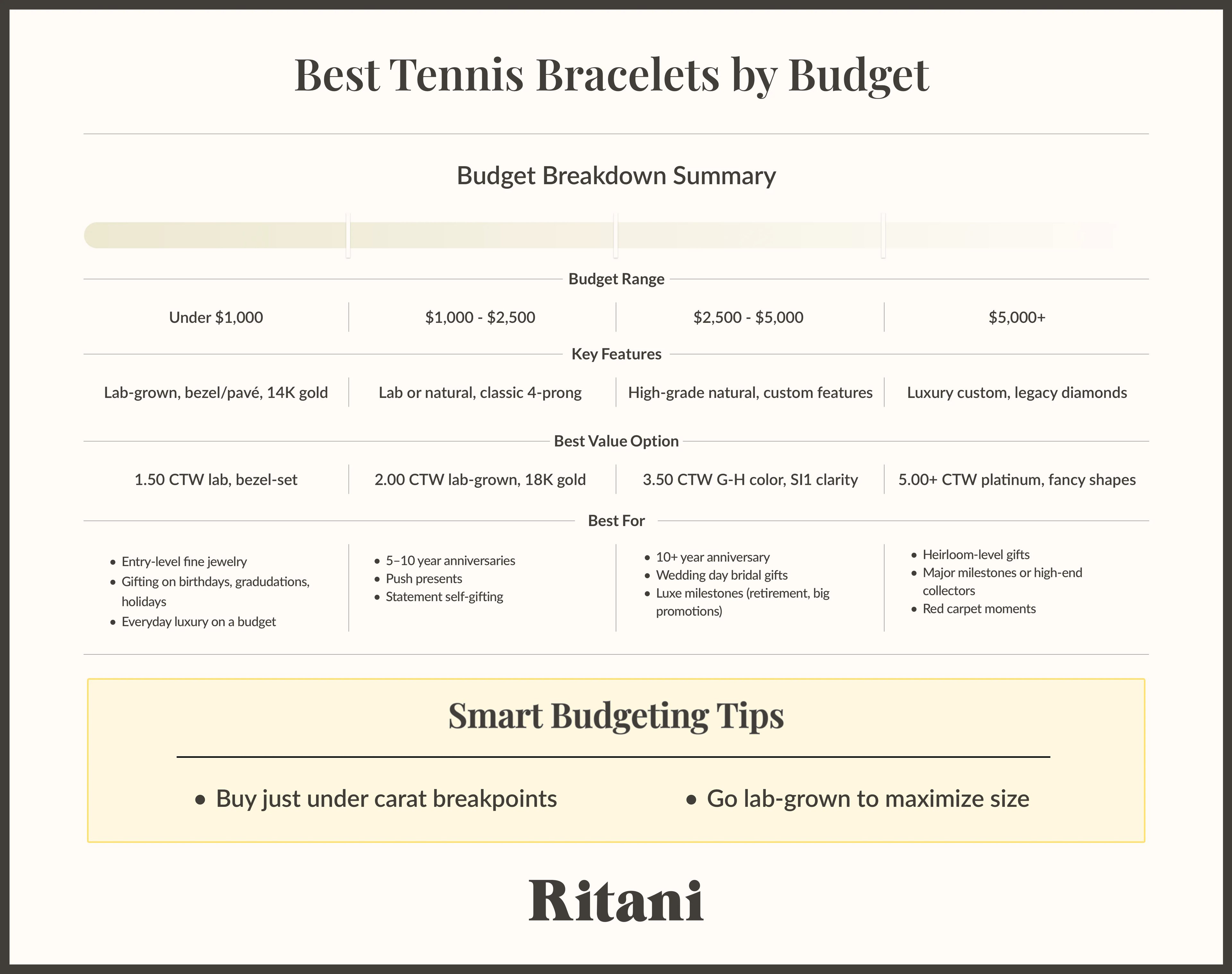

Best Tennis Bracelets for Every Budget

This guide breaks down what impacts the cost of a tennis bracelet, plus our expert recommendations for the best options across every budget—from everyday essentials to heirloom-worthy designs.

Read article

Copyright © Ritani 2026